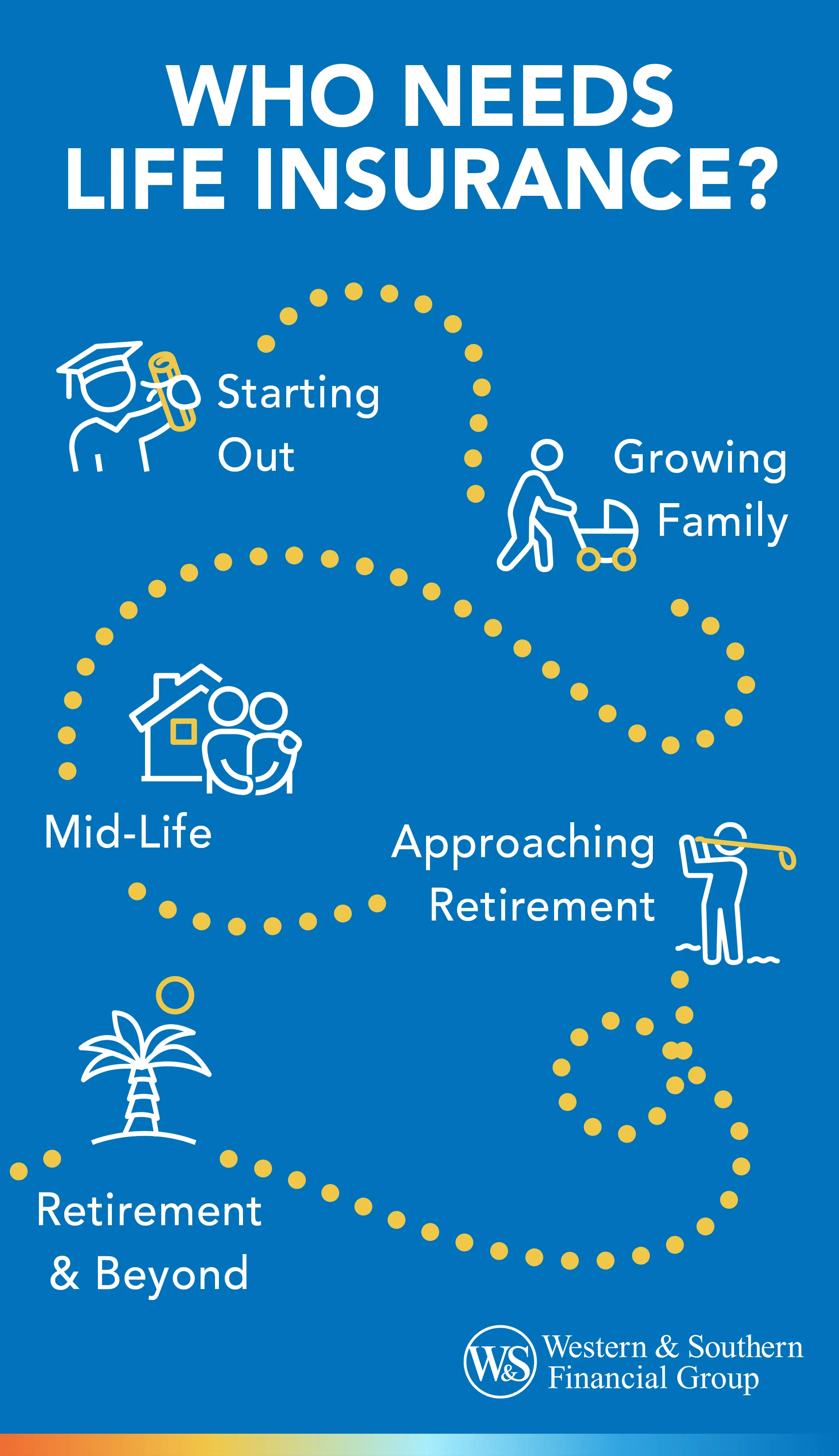

Understanding the Value of Life Insurance: Is Your Life Worth More Dead Than Alive?

Understanding the value of life insurance is crucial for making informed financial decisions. Many individuals often wonder, is your life worth more dead than alive? This question might seem morbid at first, but it highlights the importance of estimating the financial security you provide to your loved ones. Life insurance acts as a safety net, ensuring that in the unfortunate event of your passing, your family can cover expenses such as mortgages, education, and daily living costs. By evaluating your current financial obligations and future needs, you can better understand how much coverage is appropriate for your situation.

Moreover, considering life insurance is not just about anticipating death; it's also about planning for the future. It is essential to recognize the peace of mind that comes with having a policy in place. While your life may certainly not be worth more dead than alive, the financial implications of loss can be devastating for those left behind. A comprehensive life insurance policy can help maintain their standard of living, keeping them financially afloat during a challenging time. Ultimately, having this conversation and making informed choices can save your loved ones from unnecessary hardship.

5 Myths About Life Insurance That Could Cost You

When it comes to life insurance, many misconceptions can lead individuals to make poor decisions. One common myth is that life insurance is only necessary for those with dependents. However, this is not entirely accurate. Even if you're single or have no children, life insurance can cover debts, funeral expenses, and other financial obligations. Failing to secure a policy could leave your loved ones with unexpected financial burdens, emphasizing the importance of understanding your unique situation.

Another prevalent myth is that life insurance is too expensive, leading many to believe they can't afford it. In reality, rates vary based on numerous factors, including age, health, and the type of policy selected. Many people can find a suitable plan that fits within their budget. Moreover, waiting to purchase life insurance can result in higher premiums as you age or if your health declines. It's crucial to evaluate your options and consider the long-term financial impact of being uninsured.

Life Insurance 101: What You Need to Know to Protect Your Loved Ones

Life insurance is a crucial component of financial planning, providing peace of mind and security for your loved ones in the event of your untimely passing. At its core, life insurance is a contract between you and an insurance company, where you pay premiums in exchange for a death benefit that will support your beneficiaries financially. Understanding the different types of life insurance policies, such as term life and whole life, is essential to making an informed decision that best fits your family’s needs.

Moreover, here are several key factors to consider when selecting a life insurance policy:

- Coverage Amount: This should be sufficient to cover debts, living expenses, and future financial goals.

- Policy Type: Assess whether a term or permanent policy aligns better with your long-term plans.

- Premiums: Evaluate what you can comfortably afford to pay on a recurring basis.

- Beneficiaries: Specify who will receive the death benefit, ensuring they are aware and equipped to handle the funds responsibly.

By taking these steps, you can ensure that you provide lasting protection for your loved ones, demonstrating your commitment to their financial security.