Understanding the Different Types of Insurance for Your Small Business

As a small business owner, it's essential to protect your investment with the right types of insurance. Business insurance can be broadly categorized into several types: general liability insurance, property insurance, workers' compensation insurance, and professional liability insurance. Each of these plays a crucial role in safeguarding your business against various risks. For example, general liability insurance covers legal fees and settlements when your business is accused of causing harm to another party or their property. On the other hand, property insurance protects your physical assets against damage from events such as fire, theft, or natural disasters.

Understanding these insurance types is vital, as it helps you tailor coverage that fits your unique business needs. Workers' compensation insurance is mandatory in most states and covers employee injuries that occur on the job. Additionally, if your business provides professional services, professional liability insurance is necessary to protect against claims of negligence or failure to deliver quality service. For more information on selecting proper insurance coverage, you can refer to the National Association of Insurance Commissioners, which offers comprehensive guidelines on business insurance.

Top 5 Reasons Why Small Businesses Need Insurance

In today's unpredictable business environment, small businesses face a myriad of risks, making insurance an essential investment. Here are the top five reasons why small businesses need insurance:

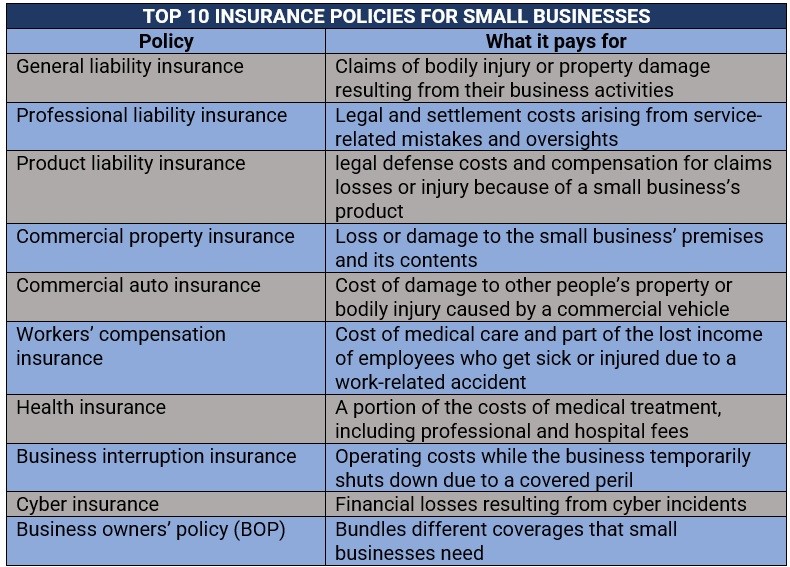

- Protection Against Liability: Small businesses can be held liable for accidents, injuries, or damages that occur on their premises or due to their products. Without adequate insurance, legal claims can lead to devastating financial losses. Understanding business liability insurance is critical for safeguarding your venture.

- Property Coverage: Insuring physical assets, such as office buildings, inventory, and equipment, protects small businesses from unexpected events like fire, theft, or natural disasters. The right property insurance can help ensure that recovery is possible after a loss. Learn more about commercial property insurance.

- Employee Protection: Providing insurance, such as workers’ compensation, helps protect employees who may be injured at work. This not only ensures the well-being of your team but also fosters a positive work environment, which can improve productivity and morale. Check out workers’ compensation insurance options for small businesses.

- Business Continuity: Business interruption insurance can cover lost income during periods when operations are disrupted, providing small business owners with a safety net. This type of insurance allows for continuity in tough times, which is vital for long-term sustainability. Find out more about business interruption insurance.

- Peace of Mind: Finally, having insurance gives small business owners peace of mind. Knowing that there’s a financial safety net in place allows entrepreneurs to focus more on growing their business rather than worrying about potential risks. This assurance is invaluable in fostering a thriving business environment.

Is Your Small Business’s Safety Net Strong Enough? Essential Coverage to Consider

For small businesses, having a strong safety net is essential to weather the inevitable storms that can arise in the business landscape. This means evaluating your current coverage and understanding what essential policies are necessary to protect your assets. Key types of coverage to consider include general liability insurance, which safeguards against claims of bodily injury or property damage, and property insurance, protecting your physical assets from events like theft or natural disasters. According to the SBA, understanding your unique business risks will help you tailor your insurance needs effectively.

Additionally, don't overlook the importance of workers' compensation insurance, which is crucial for safeguarding both your employees and your business from workplace injuries. Another crucial aspect is professional liability insurance, especially if your business provides professional services; it protects against claims of negligence or failure to deliver services as promised. Consulting resources like Insureon can provide deeper insights into the variety of coverage options available based on your specific industry needs. Ensuring these essential policies are in place can dramatically increase your small business's resilience in a challenging environment.