Understanding Whole Life Insurance: Is It Right for You?

Whole life insurance is a type of permanent life insurance that provides coverage for the entirety of the policyholder's life, as long as premiums are paid. This form of insurance not only offers a death benefit to beneficiaries but also accumulates cash value over time. Understanding how whole life insurance works is essential for assessing its suitability for your financial goals. Unlike term life insurance, which only provides coverage for a specific period, whole life insurance combines life coverage with an investment component, allowing policyholders to build savings that can be accessed during their lifetime. For more detailed insights, explore Investopedia's guide to whole life insurance.

Before deciding whether whole life insurance is right for you, consider your financial situation and long-term objectives. This policy can be more expensive than term life insurance, but it provides the advantages of guaranteed premiums and death benefits, as well as potential cash value growth. It's crucial to evaluate factors like your age, family status, and financial dependents when making this decision. Familiarizing yourself with the pros and cons can also help; you may want to review a comprehensive comparison at NerdWallet. Ultimately, choosing whole life insurance can be a significant commitment that should align with your overall financial plan.

The Pros and Cons of Whole Life Insurance: A Comprehensive Guide

Whole life insurance is a type of permanent life insurance that provides coverage for the policyholder's entire life, as long as the premiums are paid. One of the primary pros of whole life insurance is the guaranteed cash value accumulation, which grows at a steady rate over time. This cash value can be borrowed against or withdrawn during the policyholder’s life, offering a form of savings or investment. Additionally, whole life policies often come with a fixed premium that does not increase over time, providing predictability in budgeting. However, it's essential to consider the higher initial premiums compared to term life insurance, which can make it less accessible for some consumers.

On the other hand, the cons of whole life insurance can be significant for some individuals. While the policy does accumulate cash value, it often does so at a slower rate compared to other investment opportunities, which can lead to opportunity costs. Additionally, if the policyholder decides to cancel the policy, they may face surrender charges that can diminish the cash value. The complexity of these policies can also make them difficult for average consumers to understand fully, which may lead to unwise financial decisions. It's crucial to weigh these factors carefully when choosing to invest in whole life insurance.

Whole Life Insurance vs. Term Life Insurance: Which One Should You Choose?

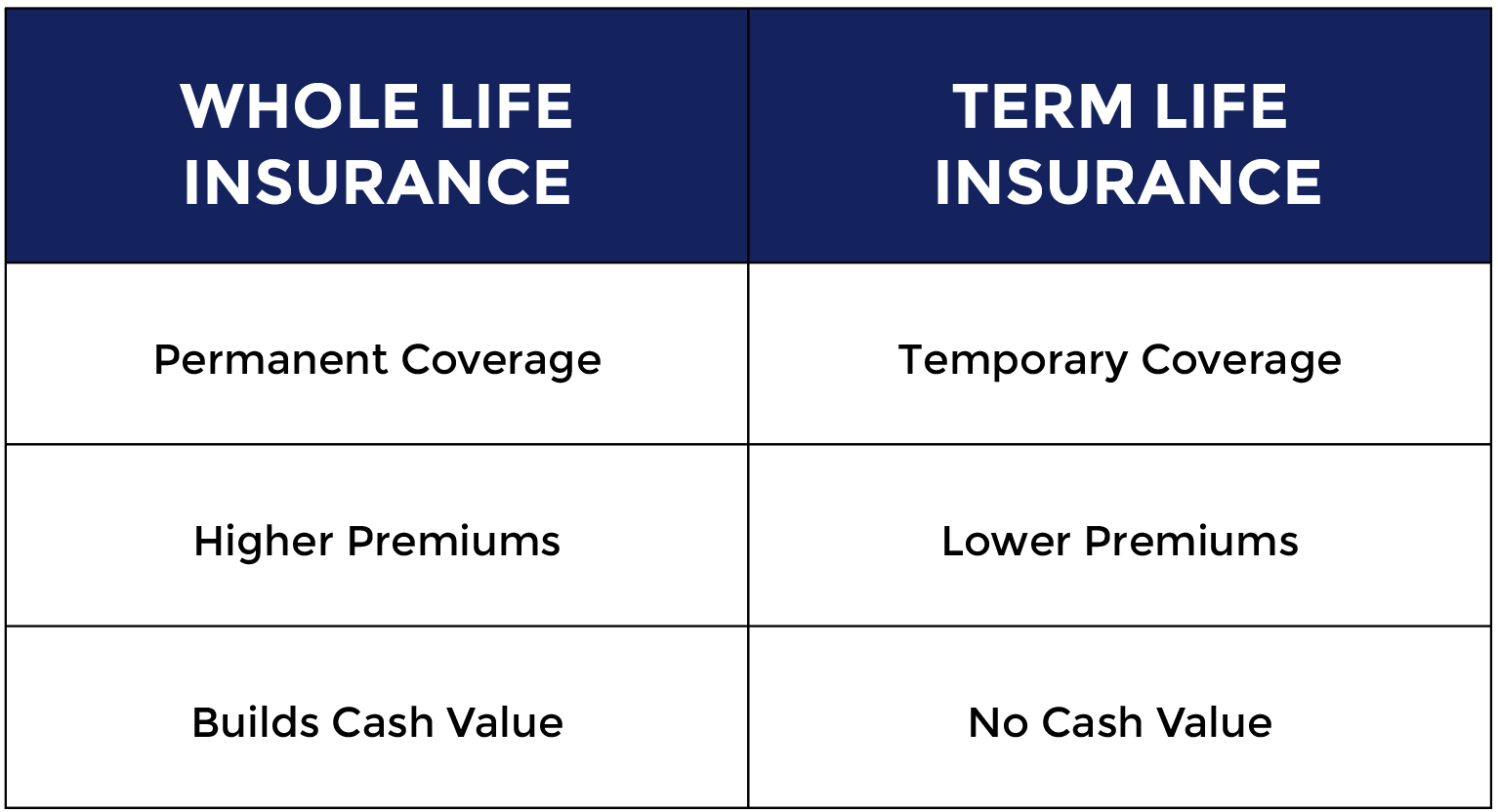

When it comes to choosing between whole life insurance and term life insurance, understanding the key differences can significantly impact your financial planning. Whole life insurance offers lifelong coverage and includes a cash value component that grows over time, allowing policyholders to borrow against it or surrender it for a cash payout. On the other hand, term life insurance provides coverage for a specified period, typically ranging from 10 to 30 years, and is generally more affordable. To make an informed decision, consider your financial goals, budget, and the specific needs of your beneficiaries. For more detailed insights, you can visit Investopedia's Whole Life Insurance Guide.

Both types of policies serve distinct purposes, and the choice ultimately depends on your circumstances. If you are looking for a permanent solution that builds value over time, whole life insurance may be ideal. Conversely, if you need affordable coverage for a specific timeframe—such as during your child-rearing years—term life insurance is often more suitable. Evaluate your needs carefully, and consider consulting a financial advisor to determine which policy aligns best with your objectives. For further comparisons, check out Forbes' Comparison of Whole and Term Life Insurance.